The global demand for energy storage systems (ESS) has surged dramatically over the past decade, largely driven by the shift towards renewable energy sources, advancements in battery technology, and government policies promoting clean energy. Energy storage systems are pivotal in balancing electricity supply and demand, ensuring stability, and optimizing energy use in grid operations. This article provides an overview of the current market share within the energy storage sector, focusing on the major types of storage technologies, their market segments, and regional trends.

1. Types of Energy Storage Technologies and Market Share

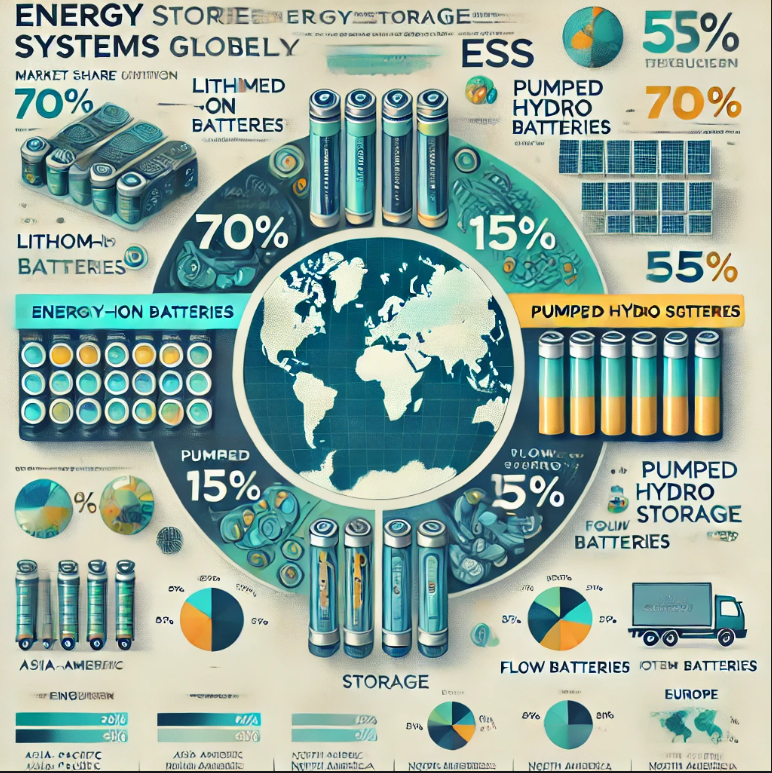

Several key energy storage technologies dominate the ESS market, each with unique applications, efficiency levels, and cost structures. The most common types include:

Lithium-Ion Batteries

Lithium-ion batteries, renowned for their high energy density and long cycle life, hold the largest market share in the ESS sector. They are widely used in residential, commercial, and utility-scale applications, capturing over 70% of the total market share. Their versatility in various applications, declining costs, and continual technological improvements make them the primary choice for energy storage.

Pumped Hydro Storage (PHS)

PHS has been the traditional large-scale storage solution, accounting for approximately 15% of the global ESS market share. Despite high upfront costs and geographical constraints, PHS remains attractive for utility-scale storage, particularly in mountainous regions with abundant water sources. It is especially popular in Europe and Asia, where legacy infrastructure supports this form of storage.

Flow Batteries

Flow batteries, including vanadium redox flow batteries, make up about 5-10% of the market. Although not as energy-dense as lithium-ion batteries, flow batteries are gaining traction in applications requiring long-duration storage, such as large-scale renewable integration. Flow battery systems are forecasted to increase in market share as innovations reduce costs and improve scalability.

Other Technologies (Thermal, Compressed Air, Flywheels)

Other energy storage technologies, such as thermal energy storage, compressed air energy storage (CAES), and flywheels, represent a smaller segment but are strategically important for specific industrial and grid applications. Combined, these technologies account for roughly 5% of the ESS market and are often utilized in niche applications or in conjunction with other technologies.

2. Market Segments and Application Share

Energy storage systems serve various segments, including residential, commercial & industrial (C&I), and utility-scale. Each segment’s adoption rate and market share are influenced by application requirements, cost, and policy support.

Utility-Scale ESS

Utility-scale energy storage holds the largest market segment, driven by the demand for grid stability, peak shaving, and renewable energy integration. The utility-scale sector commands nearly 55% of the ESS market, particularly as governments and utility companies seek to mitigate the intermittency of renewable sources such as wind and solar.

Commercial & Industrial (C&I) ESS

The C&I sector represents around 25% of the total market. C&I energy storage solutions are primarily aimed at demand charge management, power quality improvement, and backup power. High electricity costs and the availability of demand response programs make C&I storage solutions especially popular in the United States and parts of Europe.

Residential ESS

Although the smallest segment, residential energy storage is rapidly growing, representing about 20% of the market. The adoption is driven by the proliferation of rooftop solar, net metering policies, and incentives for decentralized energy solutions. Lithium-ion batteries are the preferred technology for this sector due to their space efficiency and scalability.

3. Regional Trends in ESS Market Share

- China and South Korea driving the market share. These countries are significant lithium-ion battery producers, which aligns with their high adoption rates for ESS. Japan and Australia also contribute notably to the regional market, with incentives for r

Asia-Pacific

The Asia-Pacific region leads in ESS deployment, with China and South Korea driving the market share. These countries are significant lithium-ion battery producers, which aligns with their high adoption rates for ESS. Japan and Australia also contribute notably to the regional market, with incentives for renewable integration and residential storage.

North America

North America, particularly the United States, ranks as one of the largest markets for ESS. Federal and state policies, such as California’s SGIP (Self-Generation Incentive Program), boost ESS adoption, especially in residential and C&I sectors. Additionally, grid modernization efforts and the growing need for resilience are increasing ESS deployment across the U.S.

Europe

Europe has a strong ESS market share, driven by stringent carbon reduction targets and ambitious renewable energy goals. Countries like Germany, the UK, and Italy are key players in this region, with substantial investments in both utility-scale and residential ESS solutions. Government subsidies and robust policies around energy storage and renewable integration further support growth.

4. Future Outlook and Market Dynamics

The global energy storage market is expected to grow exponentially, with some estimates forecasting a compound annual growth rate (CAGR) of 20-25% over the next decade. Lithium-ion technology will likely remain dominant, but as new storage technologies, such as solid-state batteries and advanced flow batteries, become more affordable and efficient, their market share may rise.

Government policies will play a crucial role in shaping the ESS landscape, particularly in regions with significant renewable energy targets. Moreover, the growth of electric vehicles (EVs) will influence ESS, as vehicle-to-grid (V2G) technologies enable EV batteries to function as distributed storage assets.

Conclusion

Energy storage systems are integral to the global energy transition, with lithium-ion batteries leading the market due to their efficiency and cost advantages. Utility-scale storage currently holds the largest market segment, but residential and C&I sectors are poised for rapid growth. Regional dynamics underscore the importance of policy and economic incentives in ESS adoption. As technology advances and costs continue to decline, the energy storage market share is expected to expand, enabling broader renewable energy integration and a more resilient global energy grid.